‘Buckle up’: When Millennials need to start thinking about retirement

Ideally, you would have been planning for retirement since you got your first pay, but this is how much those extra contributions can add today.

University of Sydney professor of finance Susan Thorp has a message for young Australians: “Tidy up.”

“The money that you put into superannuation in your 30s is so much more valuable in terms of compounding outcomes than the money you put in, in your 50s,” she says.

“I did a back-of-the-envelope calculation that suggested you need to basically contribute $3 in your 50s for every $1 that you would have contributed in your 30s.”

And as the oldest of the Millennials begin to hit 40, it’s time to buckle up.

Millennials need to have an eye on retirement from the very first paycheck.

Retirement planning is a conversation that financial adviser Glen Hare at Millennial-focused Fox & Hare is having more often with his clients, as their parents begin to retire.

“Many of them are witnessing their parents struggle to retire or experiencing a significant lifestyle downgrade due to poor financial planning – this can be a real eye-opener. This is often a trigger for taking retirement plans more seriously,” he says.

Doing the maths

So, is now the time for Millennials to begin thinking about retirement?

Ideally, they started thinking about retirement as soon as they began working, says Hare. “You are investing in your future from the very first pay cheque. This is your money and shouldn’t be ignored.

“For some Fox & Hare members in their 20s and 30s, superannuation is their biggest asset. The sooner they understand and take control of this asset, the greater the long-term benefits will be.”

Financial adviser Glen Hare. Steven Siewert

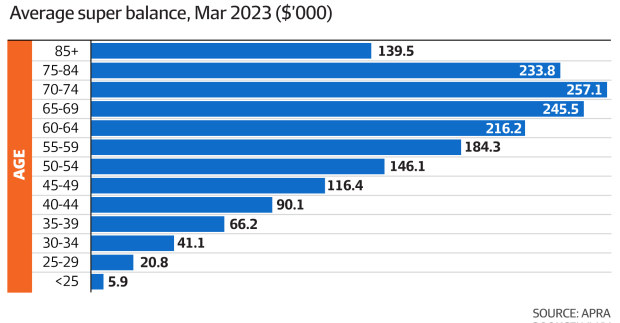

For example, if you were 30, with $41,000 in super – the average balance of those aged 30-34, according to APRA – you’d have $756,100 by the time you’re 67, according to the Industry SuperFunds super calculator, based on a $100,000 income.

But if you salary-sacrificed an extra $100 fortnightly, that would climb to $897,400 – an extra $141,300.

However, if you were 40, with the average balance of $90,100, and you started investing an extra $100 a fortnight, you’d grow your super from $589,600 to $677,800 – a smaller $88,200 difference.

And if you did the same thing at 50, you would only grow your retirement balance by $47,800.

“The average age of an advised client is 58, and most people don’t see a financial adviser until about 5 to 10 years from retirement. This is the point where people are forced to make decisions about superannuation as the desire to retire grows stronger,” says Hare.

“By this stage, the impact of advice on your quality of life in retirement is significantly limited. For Millennials, there is a huge opportunity to ensure our retirement looks exactly the way we want it to.”

What does the future look like?

He says Millennials should ideally have a clear understanding of their financial goals coupled with a proactive strategy to get there.

Questioned whether this generation is doing enough to prepare, he says “enough” is a “piece of string”.

“If you envisage nice dinners, international travel, and a degree of flexibility in your twilight years, then you’re naturally going to need a lot more than someone looking to have a “simple” retirement,” he says.

“Making additional contributions to super can be an incredibly tax-effective way to bolster your future financial means. However, this means you’ll be working with less disposable income right now – disposable income that could be used to buy your first home, start a family or travel.”

Take the Association of Superannuation Funds of Australia’s (ASFA’s) retirement calculator.

That same 30-year-old earning $100,000 with the average $41,000 superannuation balance is currently on track for a “modest” retirement, earning around $45,906 a year as a single person, its calculator claims.

To get to a “comfortable” retirement, which ASFA says requires an income of at least $50,004 a year, that same person would need to add an extra $4100 to their super a year – or $158 a fortnight.

However, Super Consumers Australia has a different take. While ASFA believes single retirees currently need $595,000 for a comfortable retirement, Super Consumers Australia believes a single retiree currently only needs $258,000 (when coupled with the Age Pension) to have a comfortable retirement.

Financial adviser at Money Planner Adele Martin agrees that for many Millennials, retirement is far from their most pressing concern.

And it doesn’t help that day-to-day cash-flow is a challenge, she adds. Many of her clients are what has been called the “sandwich generation”. They’re sandwiched between caring for young kids and, for some, elderly parents too.

“In the last six months I have seen more Millennials struggling with their cashflow … particularly those with daycare,” she says.

“They have rising interest rates, daycare fees have increased (some now more than $160 a day per child) and they are often working part-time.“

But the biggest mistake she sees people make about retirement planning is believing it has to be “all or nothing”.

“Sometimes we start with just $20 per week. It’s the habit that’s important rather than the amount. Plus due to the power of compound interest, even a small amount can add up over time.”

Chin up, there’s time

Hare says the most important thing younger savers who may be worried about their future can do right now is to just pull their heads out of the sand.

“If you’re uncomfortable with your current situation, it can be changed,” he says.

“You’ve made it this far, you’re holding down a job, you’ve mastered so many skills in life and this is just one more. Yes, the options can be overwhelming, conflicting and confusing but, if we’re being honest, which part of life isn’t?

“Making no decision, is a decision, it just may not be the best one. If in doubt, seek professional help.”

Introducing your Newsfeed

Follow the topics, people and companies that matter to you.

Find out moreRead More

Latest In Personal finance

Fetching latest articles